Protecting ATP’s business model

The low interest rates present a challenge for ATP. The low interest rates result in it becoming more expensive to guarantee and secure the real value of pensions.

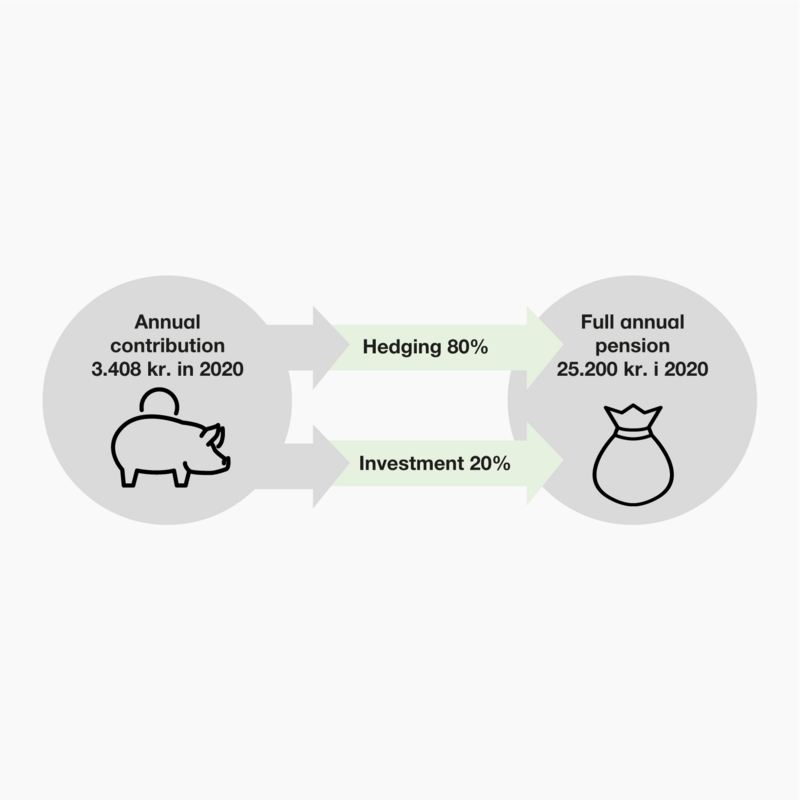

ATP Livslang Pension (Lifelong Pension) is a supplement to the state pension and is part of the common basic financial security that ensures a lifelong pension. ATP’s current business model, which sets the framework for how ATP manages and invests its members’ contributions, has historically delivered good results and received international recognition based on the hedging of the interest rate risk of the guarantees.

Over time, the business model has, among other things, ensured a predictable pension, financed the members’ increasing life expectancies and partially secured the value of the pension entitlements in real terms. The figure below provides a brief over of significant elements of ATP Livslang Pension (Lifelong Pension).

Why change ATP’s business model?

ATP’s current business model is challenged by the low interest rate environment which is expected to continue. By leaving the business model unchanged in the current interest and return environment, over time this would increase the risk of the level and real value of the members’ pensions being reduced significantly.

The first issue is that the current market interest (the way the ATP scheme works today) is critical for the pension entitlement that a member gets when making contributions. The lower the interest rate, the lower the guaranteed pensions. In a market like today, this will mean that there will be lower pension entitlement for future contributions.

The second issue is that the low interest rates, combined with general life expectancy increases, have resulted in it being more expensive to secure the real value of the guaranteed pensions. ATP’s goal of ensuring the real value of its members’ pension entitlements is met via the returns generated from ATP’s free reserves (the bonus potential) by investing in a diversified investment portfolio. The expected returns from this portfolio are in the future expected to be lower than they were historically, as the low interest rates will also have a knock-on effect on assets with projected higher returns and risks than the safer interest-based investments. Therefore, it will be more difficult for ATP to meet its objective of safeguarding the real value of the guaranteed pensions.

In order to increase the size of its members’ ATP Livslang Pension (Lifelong Pension) and also to increase the opportunities for being able to safeguard the real value of these pensions, for the past few years ATP has completed a comprehensive analysis project. The project has resulted in concrete proposals for an optimised business model for ATP Livslang Pension (Lifelong Pension) which is supported by the whole Supervisory Board and which the Danish Minister for Employment will submit to the Danish Parliament.

What is the purpose of the proposal for an optimised business model?

ATP’s optimised business model is expected to create additional value for our 5.3 million members. The objective of the proposed amendment is:

- to allow ATP to continue to provide basic financial security

- to allow ATP’s members to have the opportunity for higher pensions in real terms

- to maintain ATP Livslang Pension (Lifelong Pension) as a lifelong and guaranteed pension

- to ensure that ATP remains an inexpensive group for its members

What does the proposed amendment want to change?

The proposed amendment contains two proposed changes to the business model:

Life annuity with market exposure

Up to 25 per cent of the future guarantee contributions (20 per cent of the total contribution) can be invested in assets with higher projected returns (and risks) up until an appropriate number of years before the retirement date. ATP Livslang Pension (Lifelong Pension) will, as it currently is, be guaranteed in terms of life expectancy from the moment the contribution is made for the full guarantee contribution.

Changed hedging strategy

As a supplement to the existing interest hedging of the guaranteed pensions, it is proposed that the framework for risk taking for ATP’s hedging portfolio be changed for the purpose of allowing ATP to assume more investment risks in the long run and thus generate higher projected returns. The changed hedging strategy will not impact the guarantees.

Both proposed changes to ATP’s business model are based on an expectation that despite good and bad times and the fluctuations of the financial markets, then over time it pays off to take investment risks.

Does the proposal result in more investment-related risks?

It is only possible to generate higher returns over time by assuming more investment-related risks. For ATP, it is possible to take on more long-term risk as its members’ pension are to be paid out over the course of many yeas and because the contributions from individual years are known and cannot be moved. This means that the part of ATP’s investments that are intended to ensure that we can pay the pensions that our members have been promised can tolerate fluctuations along the way without it impacting the risk of being unable to pay the saved up pension from the retirement date.

The changes are expected to create higher pensions via investments that have higher projected returns and higher risks. This may result in ATP both seeing more gains and more losses as the financial markets fluctuate.

For ATP’s members, the projected higher returns will mean higher pensions, especially for the younger generations. Returns are achieved over time, and this is why the impact of the expected higher returns for the oldest members will be less than for the younger members who have many years to go until they reach the retirement age.

The analyses behind the proposal

ATP has made comprehensive calculations to support the proposed changes of the business model. These have been made via ATP’s stochastic projection model.

In the “ATP’s calculations and assumptions” section, there is a general overview of this projection model and the assumptions used.

Figure 1 shows the annual pension for relevant typical age groups with and without an optimised business model. For example, a 35-year-old member (born in 1985) will typically[1] get approximately DKK 17,000 in annual pension when in retirement once ATP’s optimised business model is implemented, which is an increase of 17 per cent compared to the current model.

Figure 1: According to ATP’s analyses, the changes are very likely to result in a general increase of all members’ pension entitlements over time.

[1]“Typical” is to be understood as the median outcome in the calculations.

For older members (born 1965), the effect will be less (an increase of three per cent) while for a younger member who gets the full benefits of the enhanced business model will be projected to get a pension when starting retirement that is 43 per cent higher than with ATP’s current business model.

Another way to put the proposed changes into perspective is to look at ATP’s total projected assets with and without the business model being changed. Below, figure 2 shows the projected correlation between gains and losses from the proposal and the long-term impact.

Figure 2: Overall, ATP’s assets are expected to increase by DKK 190bn over 30 years, corresponding to an annual increase of around DKK 6bn (after an additional annual pension yield tax of approximately DKK 1bn).

Do the pensions become riskier?

Life annuity with market exposure

ATP will have more investment-related flexibility for up to 25 per cent of the future guarantee contributions. This flexibility is expected to increase the members’ total pensions - but of course, also the risk of fluctuations in the total size of pensions in the period up until retirement begins. This applies up until an expected 15 years before retirement, after which point the return guarantee is phased in as the retirement date draws closer. From the time of retirement, ATP Livslang Pension (Lifelong Pension) will thus also be fully guaranteed as it is currently. As ATP must provide basic financial security, the considerations involving limiting risks up until the retirement date are weighted higher than what would presumably be a higher pension when selecting the length of the phasing-in period and the market contribution proportion.

Changed hedging strategy

With these changes, ATP will be able to assume more investment-related risks. This is needed in order to generate higher returns. However, ATP will not base its calculations on the projected higher returns when calculating its members’ pension entitlements. This means that during the time of accrual, ATP will provide its members with guaranteed pension entitlements as today, and members will subsequently be able to expect a higher mark-up of their pensions (via bonuses) than with the current business model.

ATP will maintain the interest hedging of the guaranteed pensions and the extra investment-related risks will therefore, in essence, only impact the ability to add bonuses. ATP’s calculations show that the risk of ATP being unable to meet its obligations to its members only increases from 1.4 per cent to 1.6 per cent over a 10-year period.

In the long run, the changed business model will also make it more likely that ATP can honour its commitments. This is because the accumulated returns from the changed hedging strategy are only “released” as bonuses once they exceed a certain level. ATP therefore expects that in the long run it will be in a stronger financial position than today and will be better able to weather periods of financial stress or unexpected increases in life expectancy.

ATP’s calculations and assumptions

ATP has made comprehensive calculations to support the proposed changes of the business model. These have been made using ATP’s stochastic projection model which involves a number of assumptions, for example, about future returns and interest rate levels. The assumptions are made based on realistic but conservative expectations for how the financial markets will develop.

Sådan har vi regnet – repræsentation af ATP’s balance

Af beregningsmæssige hensyn fremskrives en forenklet version af ATP’s faktiske balance.

Aktivsiden af ATP’s balance er repræsenteret ved:

- En Investeringsportefølje med eksponering som i ATP’s langsigtede pejlemærke mod de fire grundlæggende afkastfaktorer: Aktiefaktor, Rentefaktor, Inflationsfaktor og Andre faktor.

- En afdækningsportefølje med aktiver til renteafdækning af de garanterede ydelser, og i tillæg hertil aktiver med forventet højere afkast og risiko som konsekvens af ændret afdækningsstrategi.

- En portefølje, der modsvarer indbetalte og forrentede markedsrentebidrag.

Passivsiden af ATP’s balance er repræsenteret ved:

- Værdien af garanterede ydelser, der afhænger af medlemsbestanden og de tilhørende pensionsrettigheder.

- Bonuspotentialet.

- Pensionsrettigheder vedrørende livrenter med markedseksponering.

- Kapitalbuffer vedrørende ændret afdækningsstrategi.

Based on a weighing of both market expectations and the calculation assumptions used by the ‘economic wise men’ (a Danish advisory group) from 2019, ATP will calculate in the projection model that the interest rate will increase from the current very low levels and that there will still be additional returns from investing in riskier assets such as, for example, equities.

The projections use scenarios where interest rates rise and scenarios where interest rates fall. There are also both scenarios with positive returns and scenarios with negative returns. The assumptions include that ATP’s returns in the future are expected to be lower than ATP’s returns over the past five years. The assumptions are not directly comparable to Insurance & Pension Denmark’s social assumptions, but to the extent that it is possible to compare them, there is assumed a lower risk-adjusted return and lower interest rates.

Sådan har vi regnet – øvrige forudsætninger

I beregningerne stiger prisinflationen på sigt til 1,75 pct. Fremskrivningerne indeholder også scenarier med lavere og højere stigningstakter. Samtidigt antages, at bidraget alene stiger som følge af indfasningen af obligatorisk pensionsordning over de kommende 10 år.

Indbetalinger vedrørende livrente med markedseksponering investeres med et risikoniveau svarende til klassifikationen ”mellem risiko” for personer med 15 år til pensionering, jf. Forsikring & Pensions risikomærkning.

Ændret afdækningsstrategi implementeres ved at tillægge ATP’s diskonteringskurve et diskonteringsspænd på mellem 0 og 60 basispunkter, lineært voksende, samt ved at investere hvad der svarer til 15% af værdien af de garanterede ydelser i aktierisiko.